We’ve seen this morning the most recent step up within the Trump-initiated commerce warfare, with the extra 50 per cent tariffs imposed on imports from China. If the tariff insanity persists – however actually even when have been wound again in some locations (eg a few of the notably absurd tariffs on supposed US allies in east Asia, or 48 per cent tariffs on Madagascar’s vanilla) – it’s going to be extraordinarily damaging to international financial exercise within the (most likely protracted) transition. A world recession would then be the perfect forecast (via a complete number of channels together with, however not restricted to, excessive uncertainty – deadly for funding, which may normally be postponed – and wealth losses). Confronted with extreme antagonistic shocks, and excessive uncertainty, layoffs occur and corporations shut quicker than replacements emerge.

(The longer run results may also be antagonistic, reducing potential GDP in all of the international locations that take part within the “warfare”, which consciously and intentionally put sand within the wheels of their very own financial efficiency, however economies regulate – you’ll be able to have full employment in a extremely protected financial system with impaired productiveness development (see NZ within the 50s and 60s) or in a high-performing open and aggressive financial system.)

The direct results of the tariff warfare on New Zealand are nonetheless most likely fairly restricted. Our items exporters to the US face the bottom tariff band, decrease than these going through many opponents (eg European wine exporters) and the quantities concerned are only a small fraction of GDP anyway. However as just about each commentator is now declaring, the oblique results will swamp any direct results. It’s maybe a bit like early 2020 when authorities businesses have been initially targeted on the harm to some New Zealand exporters (lobster, universities and so forth) from China’s disruptions, just for these modest results to be completely swamped by the broader international results and our personal expertise with Covid (pre-emptive changes and lockdowns). In a world recession there may be just about no place to cover.

However what does, and will, it imply for financial coverage, right here and overseas (if the insanity persists)?

Within the US, it’s near-certain that there will probably be a fabric enhance in shopper costs. Headline inflation will, all else equal, enhance over the approaching few months. To the extent there may be any logic within the insanity, that’s a part of the purpose. Increased costs within the US will increase returns to home producers and make international produced merchandise comparatively much less engaging (after all, in lots of instances, US producers may also face increased prices on imported inputs). From a income perspective, it is usually akin to an enormous enhance (inefficient and all as it could be) in consumption taxes – reportedly the biggest US tax enhance in some many years. So costs will rise and actual family disposable incomes will fall.

A smart central financial institution will all the time must play issues by ear to some extent. No idiosyncratic occasion is ever fairly like one other. It isn’t inconceivable that the upper tariffs will translate into behaviours in step with households anticipating inflation to be completely increased. If that occurred, the Fed would want to lean in opposition to that danger – maintain coverage tighter than in any other case.

However an alternate state of affairs is perhaps one akin to a rise in GST. Rising consumption taxes raises shopper costs and headline inflation. We’ve had three experiments of this type in New Zealand in our post-liberalisation years: when GST was first imposed in 1986 (a 6%+ carry to the value stage) and when it was elevated in 1989 and 2010 (every rising shopper costs by a bit over 2%). On none of these events did the Reserve Financial institution search to tighten financial coverage in response, and with hindsight that was the proper name on every event. The carry in costs was (at the least implicitly) recognised by the general public as a one-off carry in inflation, that dropped out of the headline charge once more a yr later.

How seemingly is one thing like that within the US at current? Given the chaotic coverage and political processes, and the truth that – in contrast to with GST modifications – costs received’t all change on at some point, maybe there may be much less cause for optimism there. And maybe all bets are off if the general public and markets come to assume there’s a credible risk to sack and substitute present Fed decisionmakers.

However, even when family expectations (past 12 months forward) and behavior do rise – and surveys and behavior are two various things – there may be nonetheless the large hit to actual family disposable revenue to contemplate. Such hits occur with some GST changes (the NZ 1989 one was meant as a fiscal consolidation) however not others (the NZ 2010 GST change was meant as a tax change). And along with the direct results of the tariffs, there are wealth losses (see stockmarket) and the influence of enterprise disruption and enterprise uncertainty delaying funding spending. Actual exercise, and stress on sources and capability, appear virtually sure to ease. All else equal, an affordable conclusion needs to be – and market pricing is in step with this – that the Fed is extra prone to have to ease than it might in any other case have thought, in step with preserving core inflation close to to focus on.

There’s rhetoric round that someway the lesson of the previous few years is to not ease within the face of antagonistic provide shocks. However quite a bit is determined by the character of your provide shock. This isn’t (for instance) a case of actually shutting down the financial system and other people going house (voluntarily or in any other case) to keep away from a virus. The labour remains to be there, the capital gear remains to be there. It could actually all be used – capability is actual – however the demand for sources is prone to diminish fairly significantly. Financial coverage can not (after all) do something concerning the longer-term antagonistic results of a shift to a extra protectionist financial system and coverage regime. If the regime persists, People will probably be poorer than in any other case. However financial coverage typically has a task to play in smoothing the dislocations, in attempting to copy what a market rate of interest can be doing – reconciling desired saving and funding plans – absent a central financial institution. One parallel, for instance, is the recession and monetary disaster within the US in 2008/09. Financial coverage couldn’t repair the misallocation of sources and unhealthy selections that led to the monetary disaster within the first place. To the extent monetary crises impair productiveness, financial coverage additionally couldn’t do a lot about that. However not many individuals assume that merely holding the Fed funds charge at mid 2007 ranges within the face of the dislocation and related extreme recession would have made a lot sense.

What about New Zealand (and international locations like us). If we see increased costs instantly because of the tariff warfare, they need to be pretty scattered and restricted. It isn’t in any respect inconceivable that we would see import costs, in international forex phrases, falling as (for instance) Chinese language manufacturing exporters search for different markets the place they received’t face 100 per cent plus tariffs. With a reasonably restricted manufacturing sector ourselves, that phrases of commerce acquire is perhaps pretty unambiguously welcomed. We would get (quickly) decrease headline inflation and barely increased actual disposable incomes.

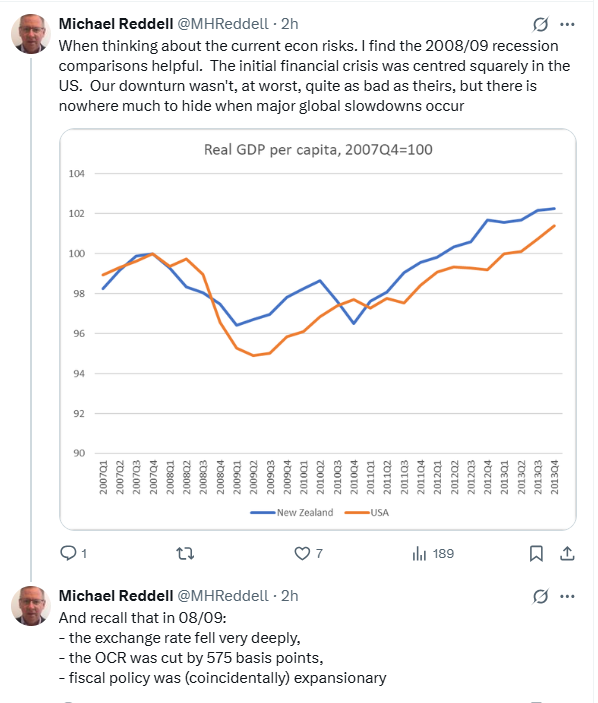

However, and then again, a world recession would virtually definitely greater than cancel out that impact. We’d see materially decrease export costs for commodities, and decrease volumes for a lot of different exports (eg tourism, college students). It doesn’t matter that the preliminary disaster/shock wasn’t generated right here, any greater than it mattered in 2008/09.

I put this on Twitter this morning

and, after all, as soon as the recession actually took maintain we received an enormous decline in (imported) oil costs but it surely wasn’t sufficient to cease the phrases of commerce general falling by 10 per cent.

Assuming the tariff insanity persists (see mercurial and unpredictable occupant of White Home) it is extremely tough to see how we – and different international locations – keep away from one thing related this time spherical. I’m glad I’m not an financial forecaster paid to place particular numbers to it – that is simply one other case of utmost uncertainty making all however probably the most extremely conditional numerical forecasts barely well worth the paper they’re written on – however the route is evident, the severity of the shock is evident, our (non-unique) publicity is evident. All else equal, the OCR is prone to have to be quite a bit decrease than in any other case, and since it’s beginning out nonetheless above impartial and with core inflation not removed from goal, that means quite a bit decrease in absolute phrases. To be clear, this isn’t a forecast, however in previous severe downturns – demand led – short-term rates of interest have typically fallen one thing like 5 proportion factors (in New Zealand, but in addition truly within the US).

The Reserve Financial institution’s MPC has its newest OCR evaluation announcement out this afternoon. They’re in a tough place: they’ve solely an appearing Governor (who was accountable for the Financial institution’s macro and financial coverage features when the actually unhealthy calls in 2020 and 2021 have been made), a deputy chief govt accountable for macro who has no experience or background within the topic, and so forth. Being an interim evaluation, they received’t have a full kind of forecasts and situations of the type carried out for the quarterly MPS. They’ve additionally continued the insanity of scheduling OCR opinions every week earlier than the CPI comes out so that they received’t actually have a good learn on the baseline – pre tariff insanity – state of core inflation. And coverage out of Washington (and Beijing and Brussels) can shift by the day.

Most individuals appear to anticipate the MPC to stay to the 25 foundation level lower foreshadowed on the final MPS. On the home macro information they’ll have at hand – all from earlier than the most recent tariff insanity (which even Jerome Powell has famous is worse than had been anticipated) – that may be completely defensible.

However so would a considerably bigger adjustment. In any case, the exterior atmosphere has modified, the impact is not prone to be small (or to be totally reversed even when we wakened tomorrow to search out the final week had simply been a nasty dream), and even the federal government, channelling Treasury, is now warning of the antagonistic financial results and dangers. It isn’t time for dramatic emergency strikes – that point might come, though one hopes we by no means have to see a 150 foundation level lower ever once more, as in late 2008 – however a charge that appeared becoming, to the New Zealand inflation outlook, 10 days in the past, shouldn’t appear proper at present. And for all that they’ve solely an appearing Governor they could really feel much less locked into Orr’s February commitments than he may need have been he nonetheless there. The dangers are fairly average, particularly as on the Financial institution’s personal estimates the OCR remains to be above impartial and the output hole is estimated to be materially detrimental.

What are some counter-arguments? There’s all the time the “six weeks doesn’t make any macro distinction” so why not wait till the (full forecasts) and the Could MPS. Maybe there will probably be fuller data. I don’t assume it’s notably compelling because it appears fairly unlikely that the fog of warfare could have disappeared by subsequent month (the macro implications will simply be beginning to change into obvious), and if a big adjustment is ultimately wanted it could be greatest to get began. If it isn’t ultimately wanted a bigger transfer at present doesn’t take the Financial institution past the place it thought issues would stage out at.

I heard one market economist on the radio this morning suggests {that a} bigger lower at present would possibly rattle individuals. Fairly most likely, however most definitely they need to be rattled. This can be a actually severe financial coverage shock Trump has launched on the world.

After which there may be the trade charge. Folks – moderately – notice that in extreme downturns the New Zealand trade charge normally falls quite a bit. That can have a tendency to lift the costs of tradables, all else equal. It hasn’t actually occurred but – if something the TWI is a bit stronger – but it surely appears a reasonably believable story. It’s simply that in severe downturns beforehand – most notably 2008/09 – the direct worth results of a decrease trade charge ended up being outweighed by the disinflationary results of the downturn on non-tradables inflation. An trade charge adjustment is prone to be a part of the general response to the tariff insanity shock, however not an alternative to motion by the MPC.

We’ll see this afternoon what the MPC has provide you with, however we shouldn’t be shocked in the event that they do lower by greater than 25 foundation factors, and doing so would most likely be the proper name. In the event that they don’t, then I suppose much more consideration than regular will probably be paid to the wording of their assertion, recognising that with the lack of a Governor some modifications in wording could be idiosyncratic – linked to at least one individual’s stylistic or different preferences.

We’ve seen this morning the most recent step up within the Trump-initiated commerce warfare, with the extra 50 per cent tariffs imposed on imports from China. If the tariff insanity persists – however actually even when have been wound again in some locations (eg a few of the notably absurd tariffs on supposed US allies in east Asia, or 48 per cent tariffs on Madagascar’s vanilla) – it’s going to be extraordinarily damaging to international financial exercise within the (most likely protracted) transition. A world recession would then be the perfect forecast (via a complete number of channels together with, however not restricted to, excessive uncertainty – deadly for funding, which may normally be postponed – and wealth losses). Confronted with extreme antagonistic shocks, and excessive uncertainty, layoffs occur and corporations shut quicker than replacements emerge.

(The longer run results may also be antagonistic, reducing potential GDP in all of the international locations that take part within the “warfare”, which consciously and intentionally put sand within the wheels of their very own financial efficiency, however economies regulate – you’ll be able to have full employment in a extremely protected financial system with impaired productiveness development (see NZ within the 50s and 60s) or in a high-performing open and aggressive financial system.)

The direct results of the tariff warfare on New Zealand are nonetheless most likely fairly restricted. Our items exporters to the US face the bottom tariff band, decrease than these going through many opponents (eg European wine exporters) and the quantities concerned are only a small fraction of GDP anyway. However as just about each commentator is now declaring, the oblique results will swamp any direct results. It’s maybe a bit like early 2020 when authorities businesses have been initially targeted on the harm to some New Zealand exporters (lobster, universities and so forth) from China’s disruptions, just for these modest results to be completely swamped by the broader international results and our personal expertise with Covid (pre-emptive changes and lockdowns). In a world recession there may be just about no place to cover.

However what does, and will, it imply for financial coverage, right here and overseas (if the insanity persists)?

Within the US, it’s near-certain that there will probably be a fabric enhance in shopper costs. Headline inflation will, all else equal, enhance over the approaching few months. To the extent there may be any logic within the insanity, that’s a part of the purpose. Increased costs within the US will increase returns to home producers and make international produced merchandise comparatively much less engaging (after all, in lots of instances, US producers may also face increased prices on imported inputs). From a income perspective, it is usually akin to an enormous enhance (inefficient and all as it could be) in consumption taxes – reportedly the biggest US tax enhance in some many years. So costs will rise and actual family disposable incomes will fall.

A smart central financial institution will all the time must play issues by ear to some extent. No idiosyncratic occasion is ever fairly like one other. It isn’t inconceivable that the upper tariffs will translate into behaviours in step with households anticipating inflation to be completely increased. If that occurred, the Fed would want to lean in opposition to that danger – maintain coverage tighter than in any other case.

However an alternate state of affairs is perhaps one akin to a rise in GST. Rising consumption taxes raises shopper costs and headline inflation. We’ve had three experiments of this type in New Zealand in our post-liberalisation years: when GST was first imposed in 1986 (a 6%+ carry to the value stage) and when it was elevated in 1989 and 2010 (every rising shopper costs by a bit over 2%). On none of these events did the Reserve Financial institution search to tighten financial coverage in response, and with hindsight that was the proper name on every event. The carry in costs was (at the least implicitly) recognised by the general public as a one-off carry in inflation, that dropped out of the headline charge once more a yr later.

How seemingly is one thing like that within the US at current? Given the chaotic coverage and political processes, and the truth that – in contrast to with GST modifications – costs received’t all change on at some point, maybe there may be much less cause for optimism there. And maybe all bets are off if the general public and markets come to assume there’s a credible risk to sack and substitute present Fed decisionmakers.

However, even when family expectations (past 12 months forward) and behavior do rise – and surveys and behavior are two various things – there may be nonetheless the large hit to actual family disposable revenue to contemplate. Such hits occur with some GST changes (the NZ 1989 one was meant as a fiscal consolidation) however not others (the NZ 2010 GST change was meant as a tax change). And along with the direct results of the tariffs, there are wealth losses (see stockmarket) and the influence of enterprise disruption and enterprise uncertainty delaying funding spending. Actual exercise, and stress on sources and capability, appear virtually sure to ease. All else equal, an affordable conclusion needs to be – and market pricing is in step with this – that the Fed is extra prone to have to ease than it might in any other case have thought, in step with preserving core inflation close to to focus on.

There’s rhetoric round that someway the lesson of the previous few years is to not ease within the face of antagonistic provide shocks. However quite a bit is determined by the character of your provide shock. This isn’t (for instance) a case of actually shutting down the financial system and other people going house (voluntarily or in any other case) to keep away from a virus. The labour remains to be there, the capital gear remains to be there. It could actually all be used – capability is actual – however the demand for sources is prone to diminish fairly significantly. Financial coverage can not (after all) do something concerning the longer-term antagonistic results of a shift to a extra protectionist financial system and coverage regime. If the regime persists, People will probably be poorer than in any other case. However financial coverage typically has a task to play in smoothing the dislocations, in attempting to copy what a market rate of interest can be doing – reconciling desired saving and funding plans – absent a central financial institution. One parallel, for instance, is the recession and monetary disaster within the US in 2008/09. Financial coverage couldn’t repair the misallocation of sources and unhealthy selections that led to the monetary disaster within the first place. To the extent monetary crises impair productiveness, financial coverage additionally couldn’t do a lot about that. However not many individuals assume that merely holding the Fed funds charge at mid 2007 ranges within the face of the dislocation and related extreme recession would have made a lot sense.

What about New Zealand (and international locations like us). If we see increased costs instantly because of the tariff warfare, they need to be pretty scattered and restricted. It isn’t in any respect inconceivable that we would see import costs, in international forex phrases, falling as (for instance) Chinese language manufacturing exporters search for different markets the place they received’t face 100 per cent plus tariffs. With a reasonably restricted manufacturing sector ourselves, that phrases of commerce acquire is perhaps pretty unambiguously welcomed. We would get (quickly) decrease headline inflation and barely increased actual disposable incomes.

However, and then again, a world recession would virtually definitely greater than cancel out that impact. We’d see materially decrease export costs for commodities, and decrease volumes for a lot of different exports (eg tourism, college students). It doesn’t matter that the preliminary disaster/shock wasn’t generated right here, any greater than it mattered in 2008/09.

I put this on Twitter this morning

and, after all, as soon as the recession actually took maintain we received an enormous decline in (imported) oil costs but it surely wasn’t sufficient to cease the phrases of commerce general falling by 10 per cent.

Assuming the tariff insanity persists (see mercurial and unpredictable occupant of White Home) it is extremely tough to see how we – and different international locations – keep away from one thing related this time spherical. I’m glad I’m not an financial forecaster paid to place particular numbers to it – that is simply one other case of utmost uncertainty making all however probably the most extremely conditional numerical forecasts barely well worth the paper they’re written on – however the route is evident, the severity of the shock is evident, our (non-unique) publicity is evident. All else equal, the OCR is prone to have to be quite a bit decrease than in any other case, and since it’s beginning out nonetheless above impartial and with core inflation not removed from goal, that means quite a bit decrease in absolute phrases. To be clear, this isn’t a forecast, however in previous severe downturns – demand led – short-term rates of interest have typically fallen one thing like 5 proportion factors (in New Zealand, but in addition truly within the US).

The Reserve Financial institution’s MPC has its newest OCR evaluation announcement out this afternoon. They’re in a tough place: they’ve solely an appearing Governor (who was accountable for the Financial institution’s macro and financial coverage features when the actually unhealthy calls in 2020 and 2021 have been made), a deputy chief govt accountable for macro who has no experience or background within the topic, and so forth. Being an interim evaluation, they received’t have a full kind of forecasts and situations of the type carried out for the quarterly MPS. They’ve additionally continued the insanity of scheduling OCR opinions every week earlier than the CPI comes out so that they received’t actually have a good learn on the baseline – pre tariff insanity – state of core inflation. And coverage out of Washington (and Beijing and Brussels) can shift by the day.

Most individuals appear to anticipate the MPC to stay to the 25 foundation level lower foreshadowed on the final MPS. On the home macro information they’ll have at hand – all from earlier than the most recent tariff insanity (which even Jerome Powell has famous is worse than had been anticipated) – that may be completely defensible.

However so would a considerably bigger adjustment. In any case, the exterior atmosphere has modified, the impact is not prone to be small (or to be totally reversed even when we wakened tomorrow to search out the final week had simply been a nasty dream), and even the federal government, channelling Treasury, is now warning of the antagonistic financial results and dangers. It isn’t time for dramatic emergency strikes – that point might come, though one hopes we by no means have to see a 150 foundation level lower ever once more, as in late 2008 – however a charge that appeared becoming, to the New Zealand inflation outlook, 10 days in the past, shouldn’t appear proper at present. And for all that they’ve solely an appearing Governor they could really feel much less locked into Orr’s February commitments than he may need have been he nonetheless there. The dangers are fairly average, particularly as on the Financial institution’s personal estimates the OCR remains to be above impartial and the output hole is estimated to be materially detrimental.

What are some counter-arguments? There’s all the time the “six weeks doesn’t make any macro distinction” so why not wait till the (full forecasts) and the Could MPS. Maybe there will probably be fuller data. I don’t assume it’s notably compelling because it appears fairly unlikely that the fog of warfare could have disappeared by subsequent month (the macro implications will simply be beginning to change into obvious), and if a big adjustment is ultimately wanted it could be greatest to get began. If it isn’t ultimately wanted a bigger transfer at present doesn’t take the Financial institution past the place it thought issues would stage out at.

I heard one market economist on the radio this morning suggests {that a} bigger lower at present would possibly rattle individuals. Fairly most likely, however most definitely they need to be rattled. This can be a actually severe financial coverage shock Trump has launched on the world.

After which there may be the trade charge. Folks – moderately – notice that in extreme downturns the New Zealand trade charge normally falls quite a bit. That can have a tendency to lift the costs of tradables, all else equal. It hasn’t actually occurred but – if something the TWI is a bit stronger – but it surely appears a reasonably believable story. It’s simply that in severe downturns beforehand – most notably 2008/09 – the direct worth results of a decrease trade charge ended up being outweighed by the disinflationary results of the downturn on non-tradables inflation. An trade charge adjustment is prone to be a part of the general response to the tariff insanity shock, however not an alternative to motion by the MPC.

We’ll see this afternoon what the MPC has provide you with, however we shouldn’t be shocked in the event that they do lower by greater than 25 foundation factors, and doing so would most likely be the proper name. In the event that they don’t, then I suppose much more consideration than regular will probably be paid to the wording of their assertion, recognising that with the lack of a Governor some modifications in wording could be idiosyncratic – linked to at least one individual’s stylistic or different preferences.

{kind=link}