The tech sell-off of 2025 has created a number of shopping for alternatives. Final 12 months, the valuations for numerous tech companies went by the roof, making it troublesome to cut price hunt. When you’ve been ready for the suitable time to leap in or add to your positions, now might be that point.

Two iconic companies particularly have seen their share costs droop thus far this 12 months: Palo Alto Networks (NASDAQ: PANW) and Nvidia (NASDAQ: NVDA). Each firms have compelling funding theses proper now, however one stands taller with larger long-term upside.

Earlier than leaping into which inventory is a greater purchase, it is necessary to first perceive the vital variations between every firm’s enterprise mannequin.

Nvidia is primarily a chipmaker that produces graphics processing items, generally known as GPUs. GPUs are specialised chips that make a ton of applied sciences potential — all the things from gaming and picture enhancing to machine studying and synthetic intelligence (AI) purposes. In a nutshell, Nvidia is a significant provider of vital parts to a wide selection of huge and rising industries, the AI trade being essentially the most promising at the moment.

Palo Alto Networks, in the meantime, could be regarded as a cybersecurity firm. Its software program delivers community safety, cloud safety, and a bunch of different safety merchandise meant to guard companies from unhealthy actors. Its product suite is spectacular, boasting greater than 80,000 enterprise prospects worldwide, with billions of protected endpoints.

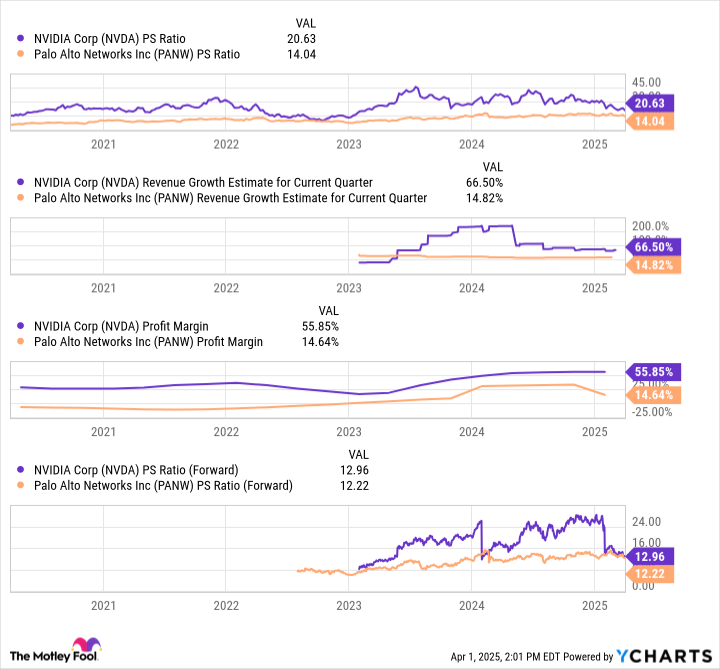

Each GPU manufacturing and cybersecurity are rising finish markets. That is evidenced by every firm’s premium valuation. Nvidia shares commerce at 20.6 occasions gross sales versus 14 occasions gross sales for Palo Alto Networks. However earlier than you suppose Palo Alto Networks is the cheaper inventory, it is necessary to verify the expansion charges of every enterprise. Wall Road analysts anticipate Nvidia to develop at greater than 4 occasions quicker than Palo Alto Networks subsequent quarter. Nvidia additionally has considerably greater revenue margins, aided by its best-in-class chips that prospects, particularly AI prospects, demand above practically each competing GPU.

As a result of Nvidia’s greater progress charges, shares commerce at simply 13 occasions ahead gross sales — solely a small premium to Palo Alto Networks’ 12.2 occasions ahead gross sales valuation. While you add in its far superior revenue margins, Nvidia appears just like the clear winner at the moment. However there’s one different cause why Nvidia is a superb wager for the following few years, and even the following few many years.

NVDA PS Ratio information by YCharts.

Nvidia is not simply driving the AI wave to progress. The corporate invested in AI early, that means its chips surpassed the efficiency of competing chips for this software a few years in the past. In reality, it was firm’s launch of CUDA — its proprietary Compute Unified Gadget Structure — means again in 2006 that has arguably given Nvidia the sting it maintains at the moment relating to chip efficiency and total market share.

The tech sell-off of 2025 has created a number of shopping for alternatives. Final 12 months, the valuations for numerous tech companies went by the roof, making it troublesome to cut price hunt. When you’ve been ready for the suitable time to leap in or add to your positions, now might be that point.

Two iconic companies particularly have seen their share costs droop thus far this 12 months: Palo Alto Networks (NASDAQ: PANW) and Nvidia (NASDAQ: NVDA). Each firms have compelling funding theses proper now, however one stands taller with larger long-term upside.

Earlier than leaping into which inventory is a greater purchase, it is necessary to first perceive the vital variations between every firm’s enterprise mannequin.

Nvidia is primarily a chipmaker that produces graphics processing items, generally known as GPUs. GPUs are specialised chips that make a ton of applied sciences potential — all the things from gaming and picture enhancing to machine studying and synthetic intelligence (AI) purposes. In a nutshell, Nvidia is a significant provider of vital parts to a wide selection of huge and rising industries, the AI trade being essentially the most promising at the moment.

Palo Alto Networks, in the meantime, could be regarded as a cybersecurity firm. Its software program delivers community safety, cloud safety, and a bunch of different safety merchandise meant to guard companies from unhealthy actors. Its product suite is spectacular, boasting greater than 80,000 enterprise prospects worldwide, with billions of protected endpoints.

Each GPU manufacturing and cybersecurity are rising finish markets. That is evidenced by every firm’s premium valuation. Nvidia shares commerce at 20.6 occasions gross sales versus 14 occasions gross sales for Palo Alto Networks. However earlier than you suppose Palo Alto Networks is the cheaper inventory, it is necessary to verify the expansion charges of every enterprise. Wall Road analysts anticipate Nvidia to develop at greater than 4 occasions quicker than Palo Alto Networks subsequent quarter. Nvidia additionally has considerably greater revenue margins, aided by its best-in-class chips that prospects, particularly AI prospects, demand above practically each competing GPU.

As a result of Nvidia’s greater progress charges, shares commerce at simply 13 occasions ahead gross sales — solely a small premium to Palo Alto Networks’ 12.2 occasions ahead gross sales valuation. While you add in its far superior revenue margins, Nvidia appears just like the clear winner at the moment. However there’s one different cause why Nvidia is a superb wager for the following few years, and even the following few many years.

NVDA PS Ratio information by YCharts.

Nvidia is not simply driving the AI wave to progress. The corporate invested in AI early, that means its chips surpassed the efficiency of competing chips for this software a few years in the past. In reality, it was firm’s launch of CUDA — its proprietary Compute Unified Gadget Structure — means again in 2006 that has arguably given Nvidia the sting it maintains at the moment relating to chip efficiency and total market share.

{kind=link}